Journal #5: A Tale of Two Economies (Part 3: Equity Market Implications)

September 2023

Greetings! The Labor Day weekend just passed, which marked the end of summer and the beginning of fall. With only four months left in the year, I have been thinking a lot about the equity markets for the next 1-2 years. Based on the macro environment that I discussed in Journals #3 and #4, I believe that the equity markets are tricky right now. In many ways, the current environment reminds me of the summer of 1999, especially in the US. Before going into more detail, it is important to review the equity framework that I use to come to this conclusion.

There are many ways to analyze a stock, but ultimately, investors can only make money from dividends and/or capital gains. The sum of these two is called the total return. Before the 1970s, dividends represented almost 40-50% of the total return of US stocks, as companies tended to pay higher dividends (4-5%). Today, with the dividend yield of the S&P 500 at only 1.5%, dividends make up a smaller portion of the total return.

Capital gains are the percentage change between the purchase price and the future selling price of a stock. For example, if you buy a stock at $100 and sell it at $120, you have a 20% capital gain. Whether it is the current stock price or future price, I like to break down the stock price into two components:

P = P/E X E

In this framework, the stock price of a company is essentially the product of its price-to-earnings (P/E) ratio and its earnings per share (EPS). For example, if the current Apple’s stock price of $192 is a product of Apple's P/E ratio is 32 and its EPS is $6 a share. (32 x 6 = 192).

To estimate the future price of Apple's stock, I think about two things:

1) Whether the P/E ratio of Apple will go higher, lower, or stay the same.

2) Whether the EPS of Apple will increase, decrease, or stay the same.

When I was in private equity about 17 years ago, this was the framework that the entire industry used to buy and sell companies (they still use the same framework today). Instead of the P/E ratio, the private equity industry uses a more sophisticated version called EV/EBITDA. Instead of EPS, they use EBITDA.

Say, I believe that the P/E ratio of Apple will stay the same at today's level of 32 times in 2025 and the current consensus estimate will be correct that Apple's EPS will go to $7.54 in 2025. Based on these, my forecasted price for Apple in 2025 is $241.28 (32 x 7.54). If my assumptions are correct, I would make an annualized price return of 12% per year for the next 2 years. (You can use a present value calculator to get to this annualized return number. I ignored Apple's dividend of about 0.5% in the above calculation.)

I would then compare Apple's potential 12% return with other stocks that I am looking at and select the ones that have a decent (not necessary the highest) return and the ones with high confidence in my assumptions.

Apple’s current EPS consensus forecast. Source: Bloomberg

In the best-case scenario, you want to buy a stock with a 10x P/E ratio and $10 EPS and sell it at a 20x P/E ratio and $20 EPS (buy at $100 a share and sell at $400). What you don't want to do is to buy a stock at a 20x P/E ratio and $20 EPS and sell it at a 10x P/E ratio and $10 EPS (buy at $400 a share and sell at $100).

Depending on the time horizon, one of these two components may not be relevant. For example, if you are a day trader with a 1-day or 1-week horizon, changes in EPS (earnings per share), which is the fundamental of a stock, should not concern you, as 1-day or 1-week earnings changes do not matter (and the company will not report them to the public). Then, 100% of your return will come from changes in P/E, which is essentially the sentiment of a stock. You simply want someone to pay you a higher price tomorrow than what you paid today because the sentiment improves. Many factors affect sentiment, such as economic news, company news, competitor news, and so on.

If your time horizon is ultra-long, say 10+ years, then changes in P/E usually do not matter as long as you buy the stock initially at a reasonable P/E. Over time, increases and decreases in P/E offset each other, and therefore, most of your price return will come from changes in EPS or fundamentals. This is the reason why Warren Buffett once famously said, "In the short run, the market is a voting machine, but in the long run, it is a weighing machine."

A tale of two markets

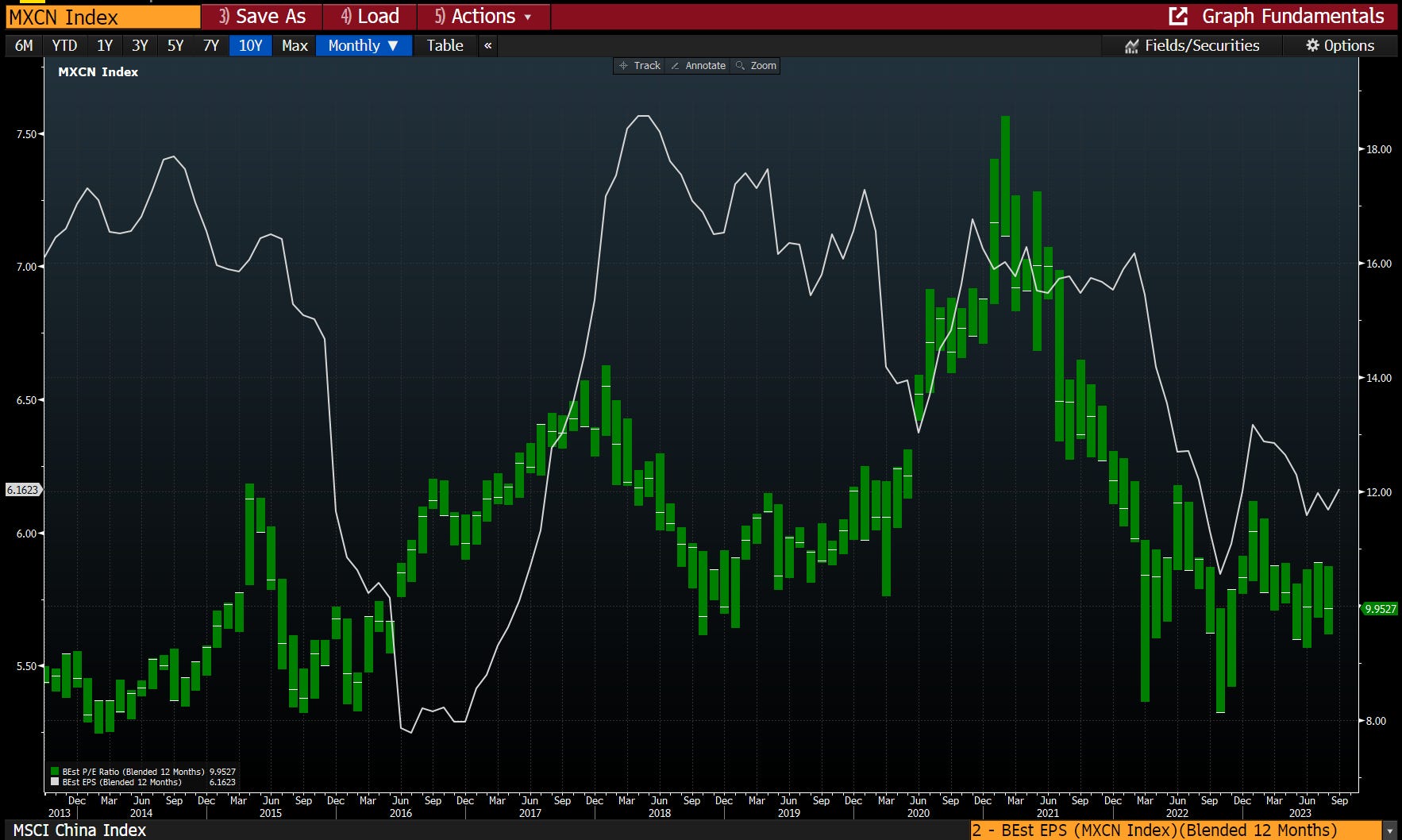

As we have a tale of two economies between the US and China, as discussed in journal #3 and #4, we also have a tale of these two markets, as shown in the two charts below. On the one hand, the US market is trading at a P/E ratio of 20x, almost at its peak level over the past 10 years (and at the higher end of its 100+ year history). On the other hand, the China market is trading at a P/E ratio of 10x, at the low end of the past 10 years. Earning trends on these markets are almost as extreme as the charts shown below. The ultimate question is where will the fundamentals and sentiment of these two markets be headed in the next two years?

MSCI China (Source: Bloomberg)

S&P500 (Source: Bloomberg)

For the US, in my view, in order for the S&P 500 to maintain a P/E ratio of 20x or higher, it requires a soft landing (or glass half full) scenario. Can the S&P 500 trade at an even higher multiple than 20x in a soft landing scenario? It is possible, but I would not bet on it. On the other hand, if a recession scenario plays out, even if it is a mild recession, we need to expect the P/E ratio to contract based on history (see chart).

Source: https://www.yardeni.com/pub/stockmktperatio.pdf

As shown in the chart below, sell-side analysts like to set a high earnings estimate first and then gradually revise it down over time. I am always puzzled by this game that they play. In a recession year, the downward revision would be even more dramatic. Given my view of the high recession risk in the US in 2024, the current earnings forecast is very likely to be revised downward, as history has shown.

Source: https://www.yardeni.com/pub/sp500squiggles.pdf

One of the greatest pieces of wisdom from Charlie Munger is, "All I want to know is where I'm going to die so I'll never go there." Since my goal is to avoid "buying a stock at 20x P/E at $20 EPS and selling it at 10x P/E at $10 EPS," and given my view of the glass half-empty scenario in the US, I have been selling my US stocks.

On the other hand, despite the overwhelming negative stories about China these days, at a P/E ratio of 10x, I am willing to continue to be patient with China stocks. In fact, the current negative stories about China are actually a bullish signal most of the time, as shown in the chart below.

China Internet

While the current very weak and uneven recovery in China will likely result in the same weak and uneven earnings recovery, I am quite confident that the worst days are behind us for the China internet sector. The government crackdown has ended, and growth for the sector should recover at a decent rate. For example, earnings for Tencent (the industry bellwether) in 2023 are likely to surpass its peak earnings in 2020, the year before the government crackdown. Other names in the sector are on the same recovery path. All of these companies are trading at a fraction of their counterparts in the US and a fraction of their 2020 peak valuation. Hence, my position in China is mainly in KWEB and similar ETFs.

Source: Bloomberg

AI Hype

Since I discussed the tech sector in China, I would like to close Journal #5 with my view on the current AI hype in the US. While there are many successful examples of first-mover advantage in technology in the past (eBay, Amazon, Uber, etc.), there are equal numbers (if not greater) of examples where the “later improvers” win.

Imagine we could travel back in time to 1995, the year the internet was born. Imagine we correctly predicted that search would be a huge winner in the internet age for years and decades to come. Even though our prediction was correct, any money we invested in any search company in the next few years would be a complete loss, because Google didn't start until September 1998 and didn't go public until August 2004. The iPhone wasn't the first smartphone; in fact, according to ChatGPT, there were at least eight smartphones years before iPhone was launched.

Hence, history has not been kind to those who overpay and buy into the hype. As the table below shows, of the top 10 tech names in 1999, only Microsoft gave you a return better than the S&P 500 for the next 22 years. For the rest, only Oracle had a return better than bonds, even though the internet was truly revolutionary.

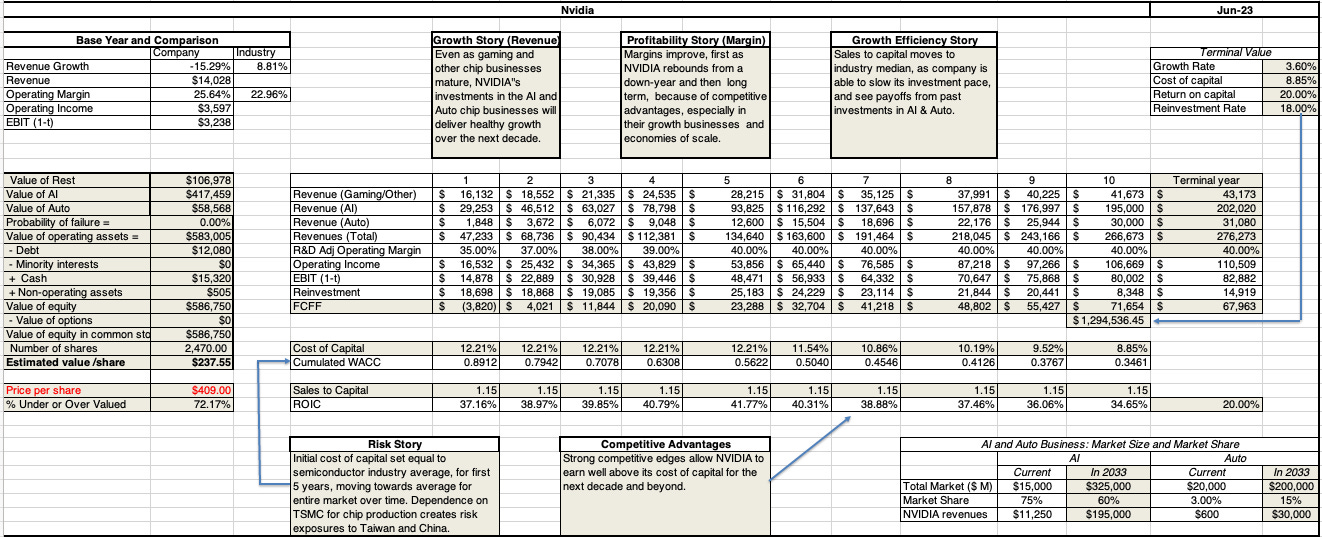

How about Nvidia? Here is the link to Professor Damodaran's (my favorite professor at NYU) detailed analysis of the company:

https://aswathdamodaran.blogspot.com/2023/06/ais-winners-losers-and-wannabes-nvidia.html

His growth assumption for Nvidia is quite generous, in my opinion. He projects revenue to grow from $27 billion in 2022 to $266 billion in 10 years (10x in 10 years; 25% CAGR). Even with this generous assumption, his intrinsic value for the company is $237 per share. In order to justify the current stock price of $460 using his discounted cash flow (DCF) model (I downloaded his Excel spreadsheet and played around with different assumptions), you would need to assume revenue of $560 billion in 10 years (20x in 10 years; 35% CAGR). However, if you were a trader, none of this would matter; sentiment on AI will drive its share price in the short term.

Source: https://aswathdamodaran.blogspot.com/2023/06/ais-winners-losers-and-wannabes-nvidia.html

Hence, this is why this past summer felt like the summer of 1999 to me. The AI hype was all around, just like the internet hype back then. Resisting the hype is very difficult. Good luck, and thank you for reading.

Great write up!