Journal #21: Trump’s Liberation Day Was Anything But Liberating

April 2025

The much-anticipated “Trump Liberation Day” has come and gone—only to be followed by significant wealth destruction, leaving few feeling liberated. To add to the uncertainty, conflicting messages from the White House have further clouded investor sentiment. The S&P 500's 10.5% two-day decline following the announcement of the reciprocal tariff policy ranks as the fifth-worst two-day drop since 1950. In this journal entry, I’ll aim to provide an objective review of the administration’s reciprocal tariff policy—its intended goals, its implications—and explore what we can realistically hope for, while also preparing for less favorable scenarios in the days and months ahead. As always, thank you for reading.

Among the Most Catastrophic Acts

Before offering an objective review of his tariff policy, allow me to first share my subjective perspective: this ranks among the “most catastrophic acts” a U.S. President could take—comparable to the infamous Smoot-Hawley Tariff nearly a century ago, as described in the following official account:

Source: https://www.senate.gov/artandhistory/history/minute/Senate_Passes_Smoot_Hawley_Tariff.htm

And yes, for those with sharp eyes—you’re absolutely right. This is a page from the official U.S. Senate website, offering its own historical view on the catastrophic damage such tariff policies have caused. Perhaps the Republican senators who currently control the Senate should ask their staff to quietly take down this webpage—before they break into chorus with Trump’s protectionist rhetoric.

So, if the Smoot-Hawley Tariff Act was considered “among the most catastrophic acts,” how bad is what Trump announced last week? The chart below from ISI shows the U.S. weighted average tariff rate over the past 100 years—and where Trump’s new policy would push that rate.

Reciprocal Tariff and Its Calculation

When Trump unveiled the first part of his two-step tariff plan during his “Liberation Day” speech in the Rose Garden—a baseline tariff rate of 10%—the U.S. equity markets actually responded favorably, rising more than 1% for a short moment, as the 10% rate came in lower than expected.

But when he pulled out the big chart (see below) to introduce the second step—his so-called reciprocal tariffs—the mood quickly shifted. Markets reversed direction and began to nosedive shortly after.

At first glance, the chart appears straightforward and logical: if China is charging a 67% tariff on U.S. goods exported to China, then it might seem reasonable for Trump to respond with a 34% reciprocal tariff—roughly half that rate.

The problem is, the numbers don't reflect reality. The 67% figure is not the actual tariff rate China imposes on U.S. goods. Prior to the 2018 U.S.–China trade war, China’s average tariff on U.S. imports was about 8%. Following the initial rounds of retaliatory tariffs, that rate rose to approximately 22.6%.

As for Vietnam, the chart claimed a 90% tariff rate on U.S. goods—when in fact, the actual average is just 8.2%.

So how did the white house get their make-up numbers? They are based on their own make-up formula as shown below:

In other words, the geniuses at the White House have tossed aside over 30 years of WTO-based tariff methodology in favor of an arbitrary formula—one based on the size of the U.S. trade deficit with a country relative to that country’s total exports. The logic seems to be: if you run a trade surplus with the U.S., you must be treating the U.S. unfairly.

In a more blunt—and frankly nonsensical—expression of this view, Peter Navarro, Trump’s Senior Counselor for Trade and Manufacturing, described U.S. trade deficits as “the sum of all cheating” the world has committed against America (source: https://www.cnn.com/2025/04/03/business/video/the-lead-peter-navarro-president-trump-tariffs-stock-markets-jobs-americans-tapper). This characterization is not just misleading—it’s absurd.

Manufacturing Revival and Tariff Revenue Boost

Following the disastrous Rose Garden announcement, the White House launched a media tour over the next two days to lay out its goals and objectives. Broadly, the administration framed its tariff policy around two key aims:

1) Manufacturing Revival – The tariffs, combined with anticipated deregulation efforts, are intended to incentivize both domestic and foreign companies to build factories in the U.S. The administration claims this could result in 1–2 million new manufacturing jobs over the next decade.

2) Tax Revenue Boost – The White House estimates that the new tariffs—particularly the 10% baseline increase—could generate $200–300 billion in annual government revenue, even before accounting for the higher reciprocal tariff rates.

Objectively, while the new tariff policy may spur some re-shoring activity, I don’t foresee a large-scale manufacturing revival for two key reasons:

1) Long-Term Investment vs. Short-Term Politics – Building a new factory is a long-term, capital-intensive endeavor—often requiring a 10+ year horizon. In contrast, the U.S. political cycle runs on a much shorter timeframe. A single recession with rising unemployment could flip Senate control in the next 18 months and shift the White House in 3.5 years. Given the stark policy swings between administrations (just compare Biden’s and Trump’s positions on Ukraine), few CEOs would commit to multi-million-dollar projects if trade policy could be reversed with the next election.

2) Labor Cost Differential – Even if the reciprocal tariff regime stays in place, the labor cost gap between the U.S. and Southeast Asia dwarfs any tariff-related savings. In Vietnam today, the average monthly wage for a garment factory worker is around $250, and about $350 for an electronics worker. That wage differential alone outweighs the impact of a 20–40% tariff in many cases. (Yes, some cost increases will inevitably be passed on to consumers, in my view. But they would still be far lower than the increases required if the factory were newly built in the U.S. Who wants a $3000 iPhone that is made in the USA? By the way, for those who still think China has cheap labor, China’s average monthly factory wage is around four times that of Vietnam.)

On the Tax Revenue Boost

It’s true that new tariffs can generate additional revenue for the government. However, any gains are likely to be offset by the broader economic fallout from those same policies. Take last week as an example: in the two days following “Trump Liberation Day,” an estimated $6.6 trillion in US market capitalization was wiped out—an economic shock that far outweighs any projected tariff collections.

Hope for the Best While Prepare for the Worst

Unfortunately, the equity markets will probabaly remain volatile. On the one hand, markets often find a bottom at the darkest hour—well before the first green shoots of recovery appear.

In fact, many technical indicators have reached such deeply bearish levels that a reversal could happen swiftly. For instance, the S&P 500’s current RSI reading of 23 (below) is exceptionally low, rare and often unsustainable.

More importantly, while the 10% baseline tariffs took effect this weekend, let’s hope that the $6.6 trillion in lost market capitalization last week—and a few cool-headed voices within the White House—will persuade Trump to reconsider before the reciprocal tariffs set to take effect on April 9 are implemented.

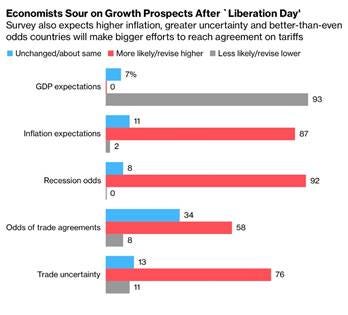

On the other hand, if Trump doesn’t change course, we should all prepare for the worst. Already, most economists at major banks are revising—or are expected to revise—their U.S. growth forecasts downward. Some firms have even shifted to making a U.S. recession their base-case scenario for 2025. Below is a Bloomberg survey of economists conducted shortly after “Liberation Day.”

Also, as Stanley Druckenmiller famously said, “the stock market is the best economist I know.” The fifth-worst two-day drop in the S&P 500 since 1950 already sends a clear signal about where the economy might be headed. If a recession materializes, S&P 500 earnings could easily fall by 15% to 20%, as illustrated in the chart below.

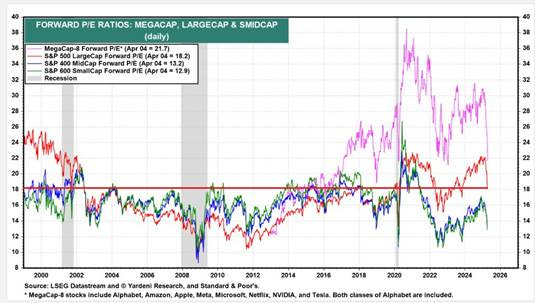

Moreover, even after last week’s sharp selloff, the S&P 500 is still trading at a forward P/E of 18x. Historically, during recessions, market valuations have tended to bottom between 10x and 14x (see below). This suggests that if Trump continues on his current path and a recession unfolds, there could still be significant downside risk ahead for equities.

Unfortunately, a recession might not even be the worst-case scenario. A stagflation scenario—driven by rising import prices—could prove even more damaging. What’s the difference? In a typical recession, we can usually count on the Federal Reserve to respond by aggressively cutting interest rates and injecting liquidity through QE to support the economy.

But in a stagflation scenario—marked by both high inflation and negative growth, something none of us have truly experienced in our adult lifetimes—the Fed’s playbook becomes far less predictable. Just how proactive and aggressive Chairman Powell can be in such an environment remains an open question in an uncharted territory.

Lastly, just a quick note on Warren Buffett. After all these years, at 94 years old, he still has the last laugh. It was just a few months ago that he was being questioned for the record cash pile at Berkshire Hathaway and had to reassure shareholders in his annual letter that he still wants to own businesses. Now, his shareholders should be thanking him once again for his investing prowess.

As always, thanks for reading.