Journal # 20: Did the AI Disrupters Just Get Disrupted?

January 2025

Greetings. Last week, President Trump announced a private-sector AI infrastructure investment initiative called Stargate, targeting up to $500 billion. Standing beside him during the announcement were the CEOs of OpenAI, SoftBank, and Oracle—the three joint venture partners expected to commit this funding over the next four years. As Trump declared, “What we want to do is to keep it in this country. China is a competitor, others are competitors. We want to be in this country…” the CEOs nodded along.

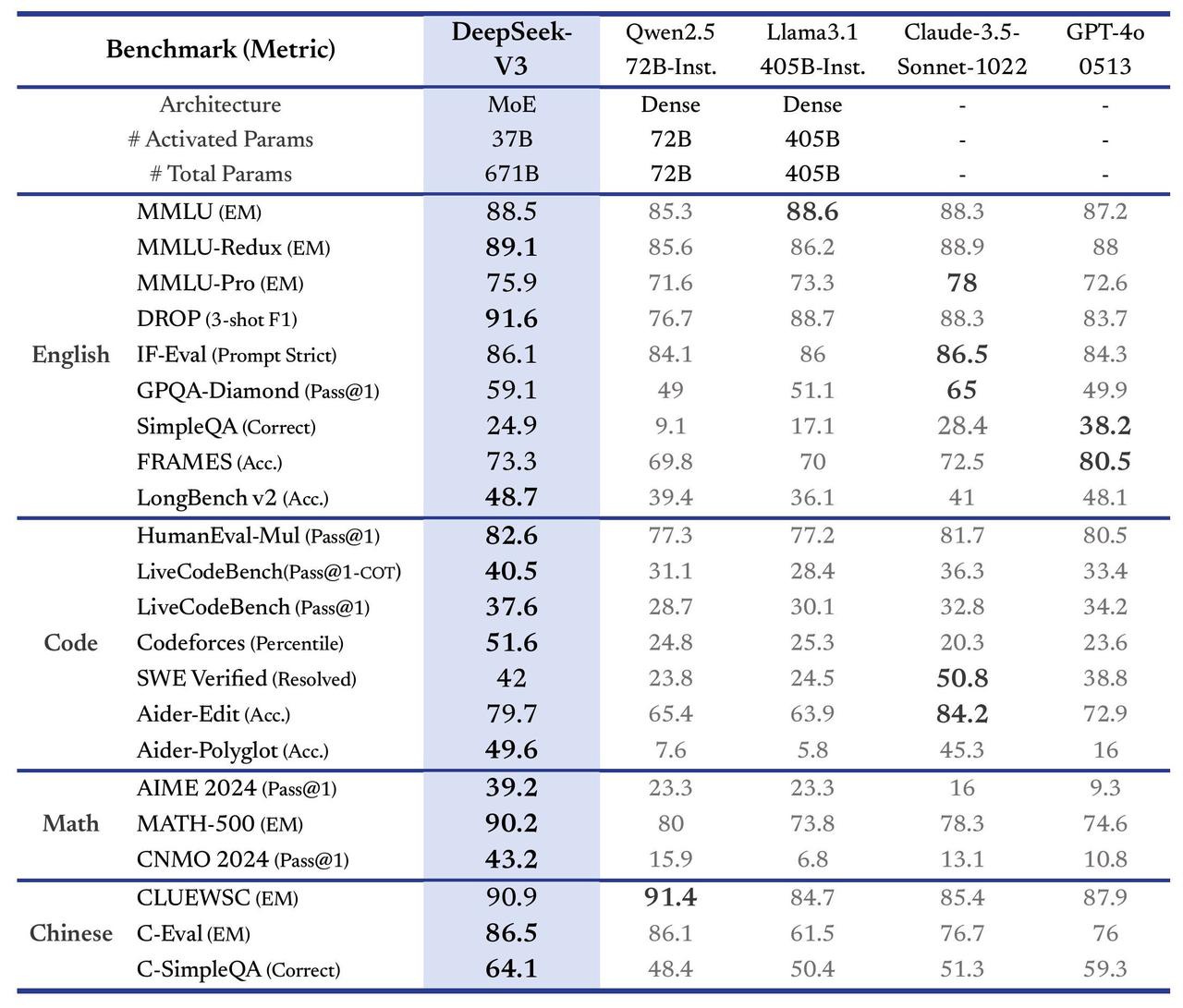

Meanwhile, a completely different but related story stole the spotlight (no, not the story about Elon saying two of the three companies don’t have the money): a small, little-known Chinese AI research lab called DeepSeek released a free, open-source large language model (LLM) that outperformed leaders like OpenAI's GPT-4o and Meta’s Llama 3.1 on several math and reasoning benchmarks. What’s more surprising? DeepSeek claims it took only two months and less than $6 million to build the model—using inferior Nvidia H800 chips.

Did the U.S. AI disruptors just get disrupted by an unknown Chinese startup? What are the implications for high-flying Nasdaq stocks? In this journal, I’ll explore these questions. As always, thanks for reading.

2022 US Export Controls on Advanced Chips

In October 2022, the Biden administration announced a set of export controls on semiconductor chips and the equipment used to manufacture them, targeting China. The Center for Strategic and International Studies called the 2022 export controls “a calculated exercise in brinkmanship designed to throttle China’s AI ambitions. Recognizing the escalating computational demands of frontier AI, reliant on thousands of the most advanced microprocessors and memory chips, the United States moved to weaponize its dominance over critical chokepoints in the global semiconductor supply chain, which China was dependent on.”

At the time, I recall having several calls with clients who asked about the implications for China. My answers to them were very general: it’s likely to slow China down, but it won’t stop it. Now, the world knows the precise answer: the export controls slowed China by 2 years and 2 months.

DeepSeek

What’s interesting is that DeepSeek wasn’t even created by a tech company but by a quant hedge fund in China, treating it as a side project. The following chart, released by DeepSeek, pretty much sums up its capabilities relative to other LLMs:

Source: https://x.com/deepseek_ai/status/1872242657348710721/photo/2

The following CNBC video also does a good job interviewing U.S. AI experts on what DeepSeek has achieved:

.

In addition, MIT Technology Review further explored how DeepSeek accomplished this: “DeepSeek’s success is even more remarkable given the constraints facing Chinese AI companies in the form of increasing U.S. export controls on cutting-edge chips. But early evidence shows that these measures are not working as intended. Rather than weakening China’s AI capabilities, the sanctions appear to be driving startups like DeepSeek to innovate in ways that prioritize efficiency, resource pooling, and collaboration.” (Source: https://www.technologyreview.com/2025/01/24/1110526/china-deepseek-top-ai-despite-sanctions/)

While the ongoing U.S.-China AI race is fascinating—especially with debates on X about whether DeepSeek truly spent just $6 million on its model and whether it uses the inferior H100 chips or smuggled advanced A100 chips banned by the U.S. government—what intrigues me more about DeepSeek are its potential economic and market implications.

Franchises vs. Businesses

In Warren Buffett’s 1991 Letter to Shareholders, he described the characteristics that distinguish a franchise from a business:

Source: https://www.berkshirehathaway.com/letters/1991.html

As investors, we naturally place a much higher value on franchises than on regular businesses. However, since 1991, Wall Street has gradually loosened Warren Buffett's definition of franchises, particularly for high-tech companies. High rates of return on capital are no longer a strict requirement, as long as the technology is compelling enough to promise high rates of return on capital at some point in the future—even if that future is decades away.

Last October, OpenAI, the money-losing nonprofit and creator of the widely popular LLM ChatGPT, raised an additional $6.6 billion at a staggering $157 billion valuation—a prime example of the loosened definition of franchises.

Source: https://www.nytimes.com/2024/10/02/technology/openai-valuation-150-billion.html

$60 meal vs $2 meal

However, DeepSeek, with its LLM comparable to OpenAI’s, now raises serious questions about the strength of OpenAI’s franchise. According to several AI developers on X, the cost to use DeepSeek’s model is only $2.20 per million tokens, compared to OpenAI’s $60 per million tokens (a million tokens represents a measure of AI model usage). The cost difference between DeepSeek and OpenAI is almost like comparing a scooter to a Ferrari.

This brings us to the market implications for DeepSeek: Imagine you invested in my 5-star, but unprofitable, restaurant last October, at a $1.5 million valuation, and my restaurant typically charges $60 per meal. This month, a new restaurant opens next door, offering the same 5-star quality food and service for just $2.20 per meal. Now, I come back to you as an investor, asking for more money to build a new kitchen to compete with this rival. Would you still invest in my money-losing restaurant? And would you still value my restaurant at $1.5 million? Or would you go across the street to my rival and invest with them?

If you doubt the viability or valuation of my restaurant now, shouldn’t you apply the same skepticism to OpenAI—and even the “Magnificent Seven” tech giants that have poured billions, and will continue to pour billions, into AI without any clear path to a return on capital for their investments?

Lessons from Global Crossing

In The World Is Flat by Thomas Friedman (one of my favorite books), he recounts how companies like Global Crossing laid massive amounts of fiber-optic cable during the dot-com bubble, anticipating exponential growth in bandwidth demand. While this overinvestment led to Global Crossing’s bankruptcy in 2002, it ultimately benefited the global economy by providing cheaper and faster internet access, which fueled innovation and growth for the rest of the tech industry for years to come.

Similarly, if training AI models becomes cheaper, faster, and easier due to advances like DeepSeek, the demand for AI development and inference will accelerate even further. Yet, as an investor, you just don’t want to be a shareholder in the next “Global Crossing,” where your capital sees no return, even if the investment benefits the world. Perhaps OpenAI should reconsider its transition to a for-profit enterprise and remain a nonprofit. For Meta, a for-profit enterprise, Zuckerberg probably needs to rethink his monetization strategies for his LLM model and create a new narrative to justify Meta’s capital expenditure plans and sky-high valuations to his investors, as the world has yet to discover how many other DeepSeeks exist in China.

As always, thanks for reading.

Hi Daniel,

Hope you enjoyed the Holidays & New Years. I recall from a few journal entries ago where you quoted a SF VC firm saying there is a $500 billion hole of profits needed to cover the current Capex investments from these US tech companies. Seems like that point you made is being played out as the market is now skeptical on those heavy AI investments.

This news on DeepSeek was negative for US Tech, but how do you see this affecting the underlying businesses of any Chinese Tech stocks, if any?

I learned a lot from Aravind Srinivas on the CNBC interview. And your analysis and reasoning is impressive. Thank you! 🙏